Here’s some Context:

We’re currently 35 and 36, and have one child who is 17 years old. We’re originally from the US and are living overseas, rent-free. We have no debt, but we do use credit cards for travel rewards and pay them in full each month.

Our monthly expenses are <$2,500 and include the following:

- Utilities: electricity, water, internet

- Mobile phones

- Food (groceries + eating out)

- Transportation

- Miscellaneous (clothing, home purchases, gifts, etc.)

First Quarter Travel:

Australia, US (for a family emergency)

Here’s What Happened this Quarter:

- UM. COVID-19 happened. Thanks, 2020.

- In February and March, our travel plans were interrupted due to COVID-19. Travel plans are now (understandably) canceled for the foreseeable future.

- Our teenager’s International School closed early March and moved to online learning.

- We spent most of March debating whether we go ahead with scheduled travel plans, changing travel plans, cutting trips short, etc.

- Our family decided to stay abroad rather than return to the US.

- We spent the rest of the month 100% focused on staying safe + healthy.

A little more about our situation regarding COVID-19

Mr. Unsettled’s job is secure, although it’s been a challenging time for him at work due to scheduling, being short-staffed, etc. Ironically he’s been busier than ever and sadly, hasn’t been able to work from home. This isn’t ideal, of course, but thankfully none of us are in high-risk so we have been able to stay healthy (so far…knocking on ALL THE WOOD) by creating strict routines and taking precautions. We’re talking no public transportation, no crowds, wearing masks everywhere, staying home 99% of the time. And because he was leaving home anyway, Mr. Unsettled took on any errands outside of home.

These are uncertain times, and we consider ourselves so incredibly lucky. We know it’s been hard on millions of families around the world, many in our own expat community. People are losing jobs; families are separated; companies are canceling expat contracts and sending their employees home — with little notice — in the middle of a pandemic. For now we’re counting our blessings while keeping in mind that anything could happen. As expats, we’re in an especially precarious situation because we’re living in a country that is not ours. If Mr. Unsettled were to be laid off, we can’t legally stay here. And we also couldn’t easily leave if required. Thankfully that seems unlikely, but we’ve spent a lot of time over the past few months evaluating what our back up plan will be if that were to change.

As for the US economy as a whole, we’re not panicking. We ignored the markets when they crashed back in March, and are basically ignoring them as they’ve rebounded. Our attitude is that things are going to get much worse before they actually get better. Here’s what we’re doing to give ourselves a little peace of mind:

We shifted from investing in the market to saving cash just in case.

Our goal is to have at least $100,000 in cash savings before re-evaluating. We already had 6 months of income in cash as well as credit cards with fairly high limit s($30,000+) so felt fine with our level of emergency savings. But 2020 is no joke and we want to be extra, extra conservative.

For now we’re pausing all real estate investing.

We are still saving >$3,000/month earmarked for this purpose (that we could dip into in an emergency) which is included in the cash number below. Our second property’s closing has been delayed due to COVID-19, but we will be closing on our second property in April. Besides wanting to keep as much cash on hand as possible, it’s nearly impossible to close on properties overseas with the US Embassy closing, etc. We hate to slow down after buying our first two properties in 6 months, but we’re anticipating possible deals towards the end of 2020/early 2021 so are fine waiting.

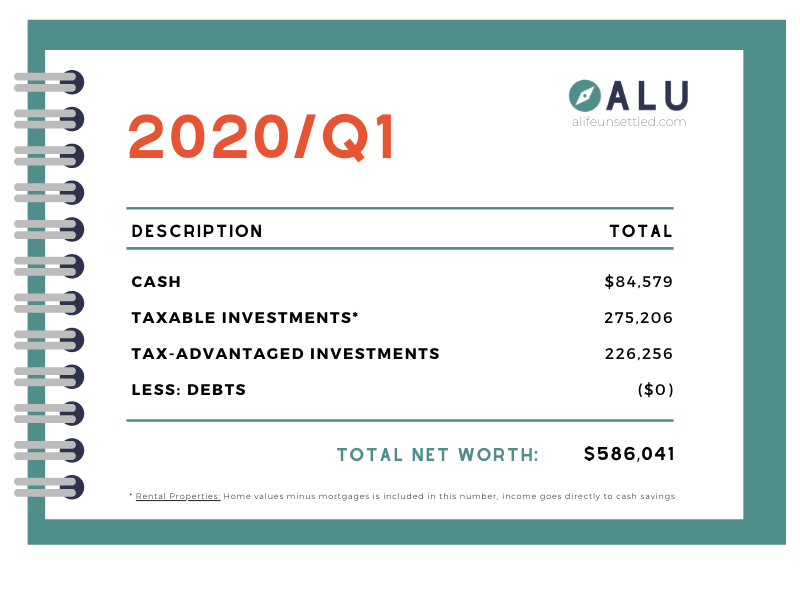

Here’s how our financial picture looked at the end of 2020/Q1:

And because it’s always nice to see the change over the previous quarter, here’s the change from 2019 Q4:

Cash ($6,509)

Taxable Investments* ($25,398)

Tax-Advantaged Investments ($64,132)

Debt: $0

Total Change: ($96,039)

OUCH.

But we’re not panicking! Other than the changes I listed above, we’re not doing anything different! We’re just riding it out. Have I mentioned that we’re not panicking?!

If we’ve learned anything in the past few months it’s that the most important thing we can be is safe + healthy…and we are.

So whatever the rest of 2020 brings, we’ll be ready.